Reading time: 4 minutes

Emergency Lighting Is No Longer Just a Compliance Box. It Is Becoming a Smart Building Differentiator

Digital connectivity, new technologies, and rising requirements are transforming emergency lighting into an integral component of modern building and safety strategies.

Emergency lighting has traditionally stayed in the background of building design. It is installed to meet code, tested periodically, and rarely discussed unless something goes wrong. That is now changing. Based on recent global market analysis by Frost & Sullivan, emergency lighting is entering a new phase shaped by regulation, digitalization, and the rising complexity of modern buildings.

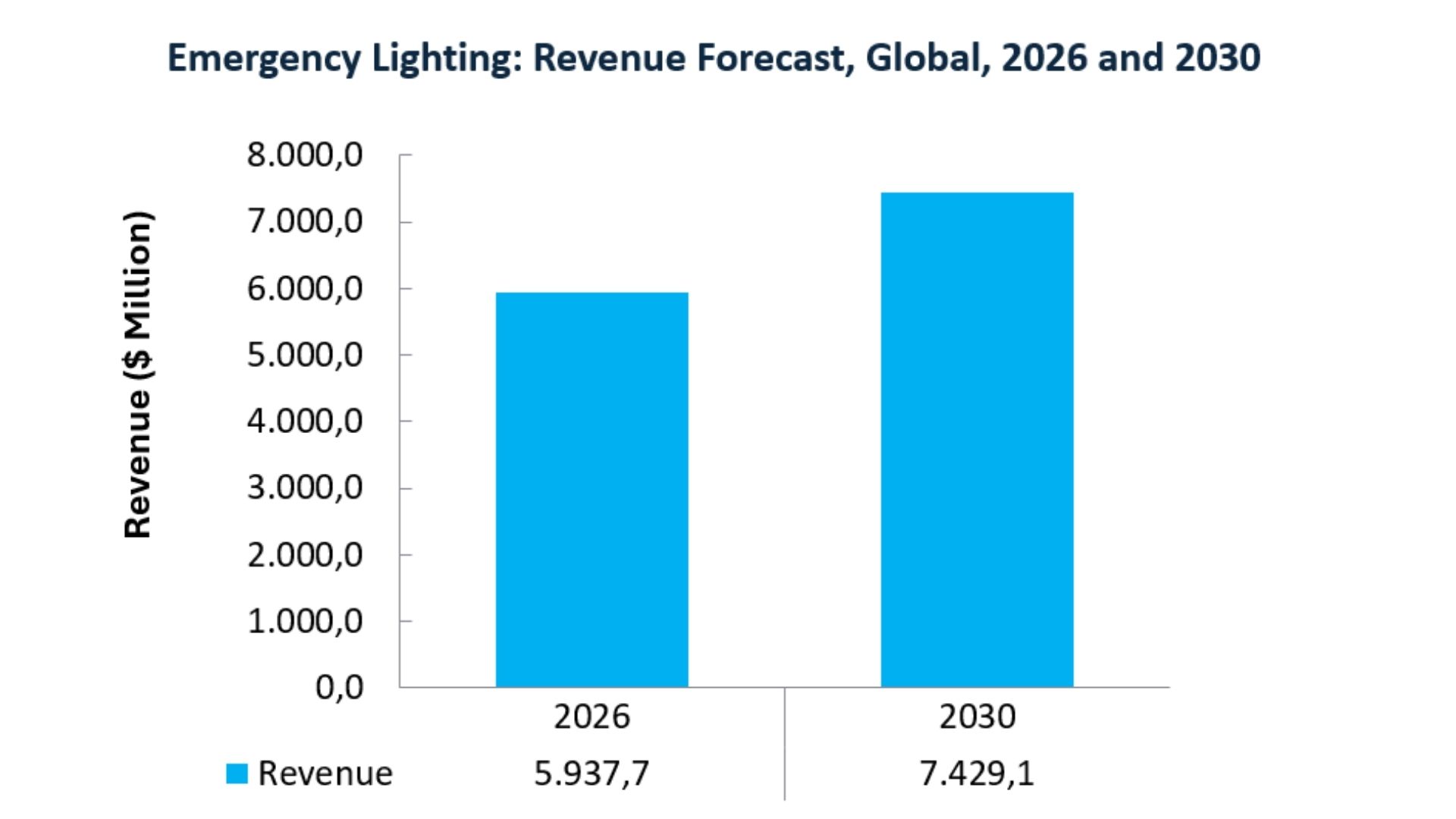

Between 2024 and 2030, the global emergency lighting market is expected to grow steadily, reaching more than US$7.4 billion by the end of the decade. While this may look like moderate growth, the real story lies in how the market is evolving. Emergency lighting is shifting away from static, stand‑alone products toward intelligent systems that actively support life safety and building performance.

Why Growth Is Getting Harder Even as Demand Increases

Demand fundamentals remain strong. Stricter fire and life‑safety regulations continue to mandate emergency lighting in commercial and public buildings. Construction and renovation activity is also supporting the market, especially in hospitals, data centers, transport hubs, and large commercial developments.

At the same time, suppliers face growing pressure. Competition is intense, with more than a thousand active players globally. Low‑cost emergency signage continues to challenge pricing, particularly in cost‑sensitive markets. Customers are also asking for more value, including lower maintenance costs, better energy efficiency, and digital monitoring capabilities that reduce manual testing.

This combination of rising expectations and margin pressure is forcing vendors to rethink how they compete and differentiate.

Technology Is Redefining Emergency Lighting

Technology is playing a central role in this transformation. Wireless communication, IoT connectivity, and cloud‑based monitoring are turning emergency lighting into a connected system rather than a passive installation.

Manual testing and paper compliance logs are increasingly being replaced by automated self‑testing, fault alerts, and centralized dashboards. Wireless technologies and IP‑based controls make it possible to monitor system health in real time, predict failures, and reduce maintenance effort. For building owners, this means lower operating costs and improved reliability.

Another important shift is the growing adoption of low‑power emergency lighting systems. These solutions sit between traditional self‑contained units and large central battery systems. They offer simplified wiring, safer low‑voltage operation, and greater flexibility for renovations. For schools, retail spaces, and medium‑sized commercial buildings, this approach is becoming especially attractive.

Adaptive Evacuation Is Moving Beyond Static Exit Signs

One of the most forward‑looking developments in the market is adaptive evacuation. Unlike conventional exit signs that always point in one direction, adaptive systems can change dynamically based on real‑time conditions.

In the event of fire, smoke, or localized hazards, adaptive emergency lighting can guide occupants away from danger and toward safer exits. These systems integrate with fire detection, alarms, and building management platforms to improve evacuation speed and safety.

Adoption is still at an early stage, but regulatory frameworks in Europe and North America are beginning to recognize these technologies. As awareness grows, adaptive evacuation is expected to become a key growth area over the next few years.

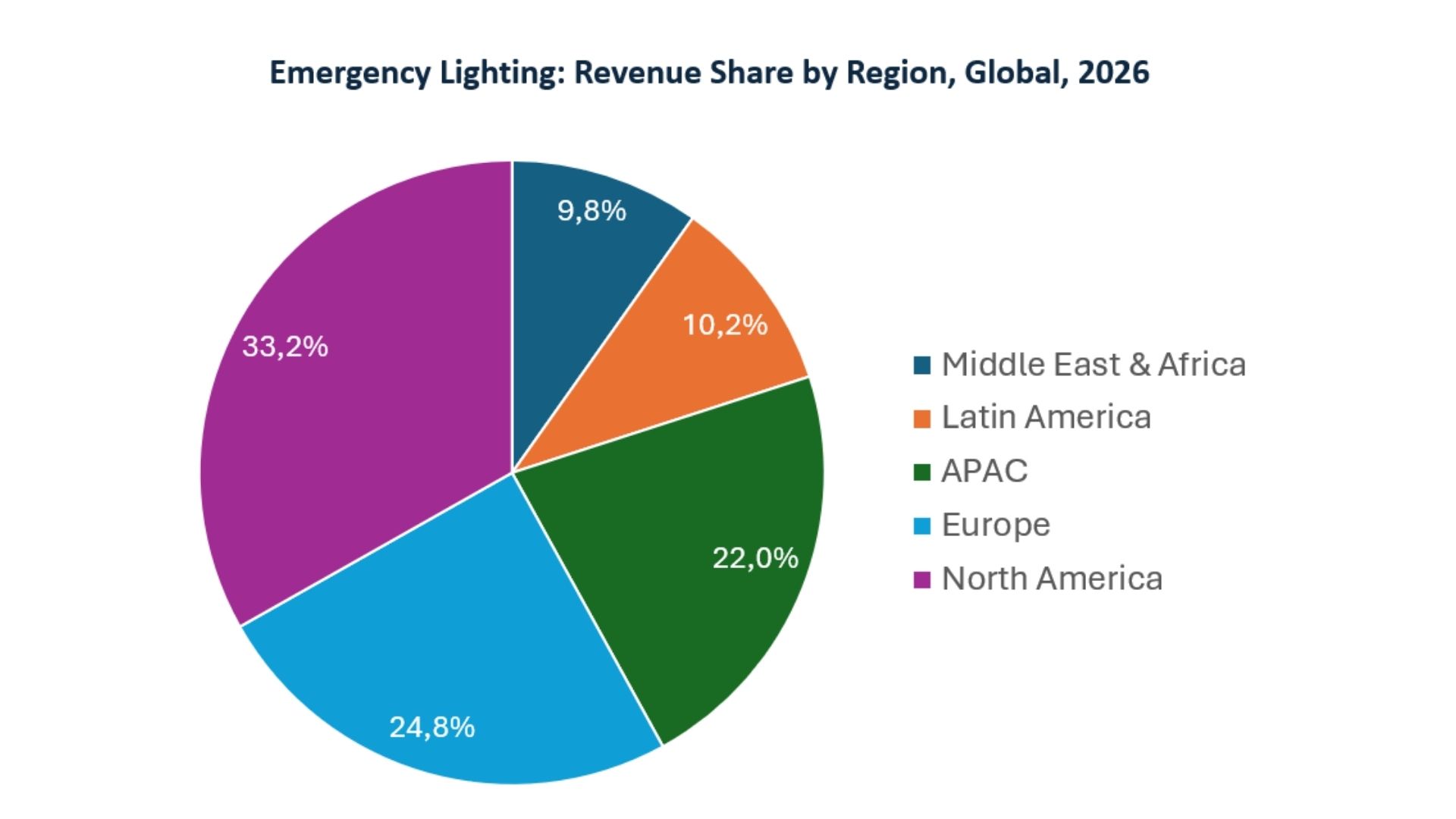

Regional Growth Tells Different Stories

From a regional perspective, Asia‑Pacific stands out as the fastest‑growing emergency lighting market. Urbanization, infrastructure investment, and tightening fire safety regulations are driving demand across the region. Europe and North America remain mature but stable markets, supported by retrofits, digital compliance, and sustainability initiatives.

The Middle East, Africa, and Latin America offer longer‑term potential through large infrastructure projects and improving regulatory enforcement. Across all regions, high‑growth end‑user segments such as data centers, healthcare, education, and industrial facilities are becoming priority targets for suppliers.

A Strategic Market, Not Just a Technical One

Emergency lighting is no longer just about luminaires and batteries. It is increasingly about software, data, interoperability, and long‑term service value. Companies that succeed will be those that move beyond compliance‑driven selling and position emergency lighting as a critical part of smart, resilient, and future‑ready buildings.

Emergency lighting is stepping out of the background. It is becoming smarter, more connected, and far more strategic than most people realize.