Reading time: 4 minutes

Corporate AI investment reached $252 billion globally in 2024, and the global AI market is projected to surpass $244 billion in 2025 alone. For building managers, this shift matters not because of the headlines, but because of what it means for the systems, services, and suppliers you work with every day and it is the context that building managers need to understand.

Why Building Managers Need to Understand AI Now

AI in commercial buildings is not yet a solved or mature technology. It is a rapidly developing field where vendor claims frequently outpace independently verified results, where the buildings most in need of AI assistance often lack the data infrastructure to support it, and where the difference between a well-chosen deployment and a poorly evidenced one can mean the difference between meaningful energy savings and wasted capital.

The analysis that follows draws on Memoori’s third edition of its Artificial Intelligence in Smart Commercial Buildings research. It is designed to cut through the noise and give building managers a clear, evidence-based picture of where AI is genuinely delivering value today, where it is falling short, and what a realistic path forward looks like.

The headlines will tell you artificial intelligence is everywhere. The evidence tells a different story, and for anyone working in commercial real estate or smart buildings, the gap between those two things is exactly where the real opportunity lies.

Memoori has published the third edition of its Artificial Intelligence in Smart Commercial Buildings research. Here’s what you need to know.

The Artificial Intelligence Adoption Gap Is Real, and Getting Wider

As mentioned above, Corporate AI investment hit $252.3 billion globally in 2024. Earnings call mentions of artificial intelligence have jumped from around 25 per quarter per firm in 2022 to over 300 today. By almost every measure, the AI hype wave is enormous.

But here’s the thing: not much of this is flowing into commercial building operations in any meaningful way. Artificial intelligence in buildings is predominantly edge-deployed, data-constrained, and operationally focused. It still relies on traditional machine learning far more than large language models. It is a different world from the generative AI dominating investment headlines.

And within buildings specifically, the adoption picture is poor. JLL’s survey of over 1,000 CRE professionals found that 92% are piloting or planning artificial intelligence, but only 5% are achieving their targeted outcomes. Deloitte’s 2026 CRE Outlook, drawing on 850 C-suite executives across 13 countries, found that the proportion reporting “transformative impact” from AI collapsed from 12% to just 1% in a single year, while those citing implementation challenges nearly doubled to 27%. That’s not stagnation, that’s regression.

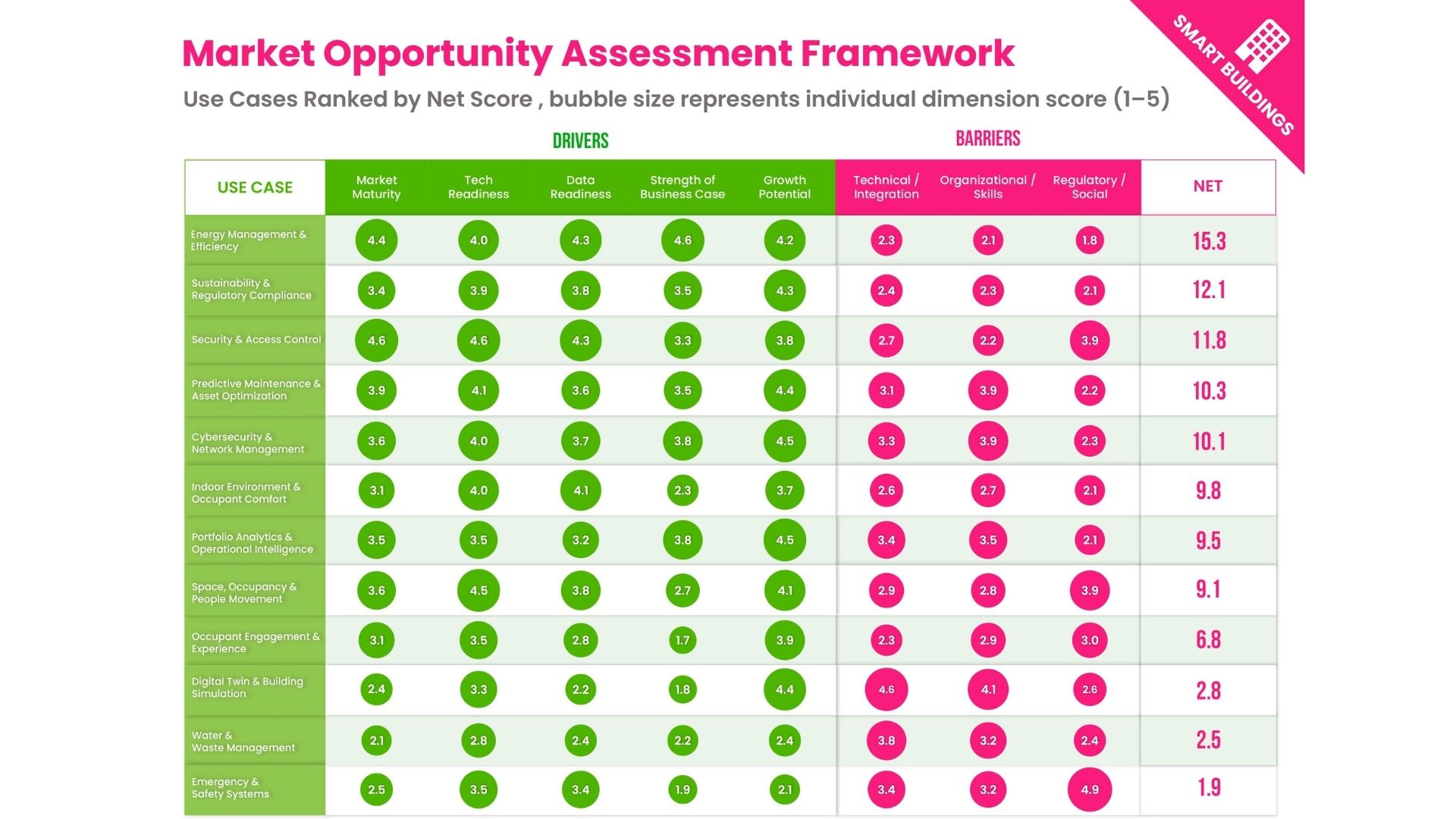

Where Is Artificial Intelligence Actually Creating Value?

Our assessment framework scores 12 application domains across five market driver dimensions and three barrier categories. Right now, only one domain sits in the top “ready for scaled deployment” tier: energy management and efficiency.

Even here, the hierarchy matters. Passive dashboards deliver around 2–3% savings, fault detection around 9%, and genuine autonomous supervisory control reaches 12–13% in independently evaluated programs. The gap between alerting a facilities manager and autonomously correcting a fault is not marginal; it is order-of-magnitude.

Close behind are sustainability and compliance, security and access control, and predictive maintenance, each with a compelling near-term case, but each with distinct barriers that the report examines in depth across all 69 use cases.

The Energy Savings Gap Nobody Talks About

One of the most important pieces of research in this report is our cross-source analysis of artificial intelligence energy savings evidence, over 40 independent studies covering more than 14,000 verified sites.

The finding is consistent. Vendor-reported AI energy savings typically fall in the 20–50% range. Independent evaluators consistently find 3–15%. NYSERDA’s Real-Time Energy Management program, covering 654 sites, found that vendor-reported savings were roughly double what independent measurement confirmed.

This isn’t just a transparency issue, it’s a procurement problem. A lot of what gets labelled as AI-driven savings turns out to be coming from program-wide upgrades, motor replacements, or full retrofits, not from the artificial intelligence component itself.

For anyone procuring AI-based energy optimization solutions for buildings, that distinction matters enormously. report grades every performance claim against an explicit evidence framework, making it a practical tool for procurement teams doing due diligence.

The Digital-Physical Gap

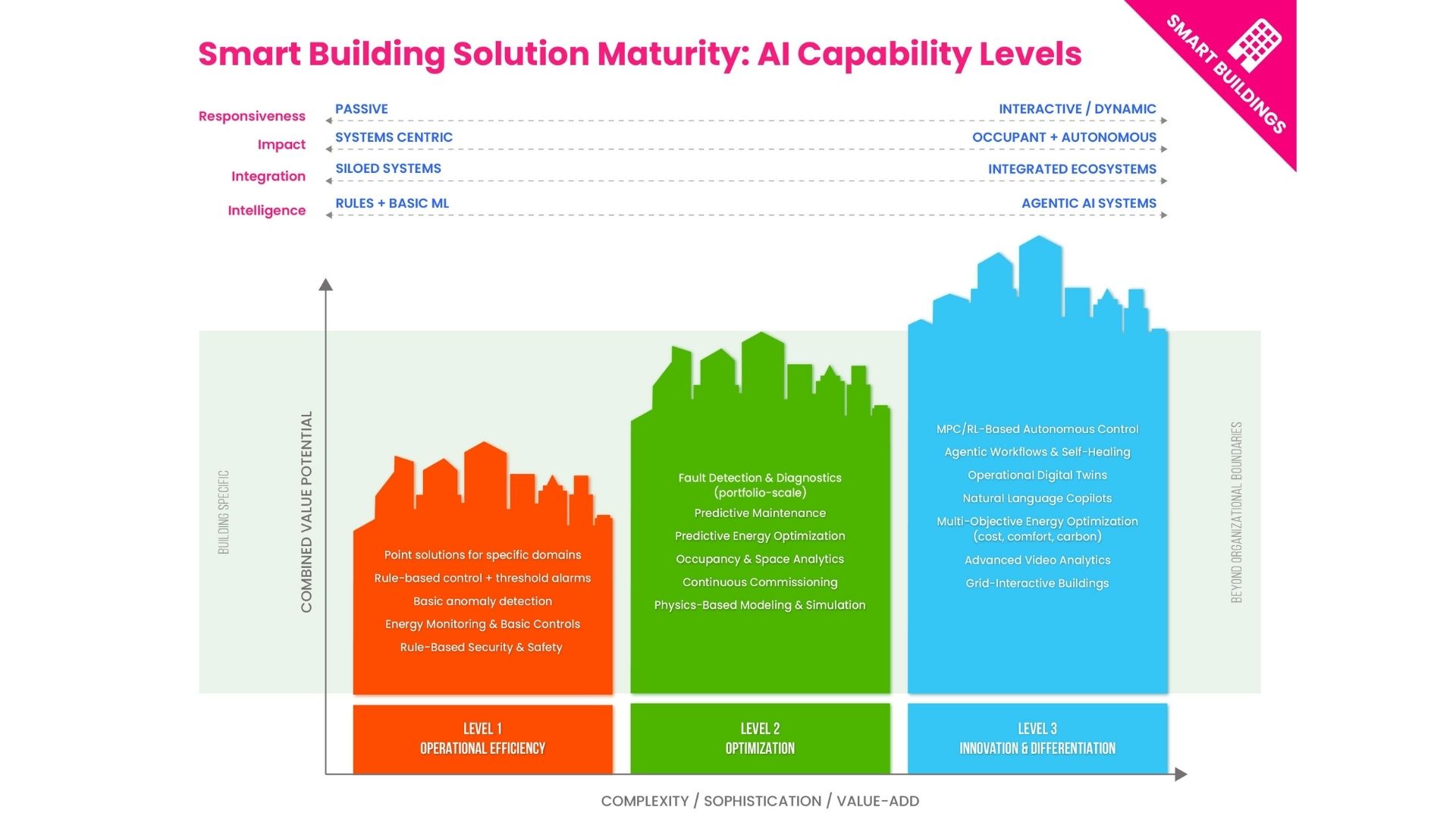

Artificial intelligence’s digital capabilities are accelerating at a remarkable rate. Software coding benchmarks have improved from around 4% accuracy in 2023 to over 80% today. But translating that into the physical world, autonomous HVAC control, multi-system building management, is a fundamentally different challenge.

As of early 2026, there is no confirmed evidence of autonomous multi-system building control in production deployment anywhere. Each additional increment of reliability requires a massive engineering effort, and in buildings, where sensor data is noisy, systems degrade, and consequences are slow to appear, that progression is much slower than in purely digital domains. As one framing puts it: bits are a million times easier than anything that touches the physical world.

The Paradox at the Heart of the Market

Perhaps the most important structural challenge for artificial intelligence in buildings is this: 87% of commercial buildings have no digital systems at all. 94% of US commercial buildings are under 50,000 square feet, and only 13% of those have any building automation system.

The buildings that most need artificial intelligence are precisely the ones with the worst data to support it.

This reality isn’t changing quickly. Memoori’s deployment forecast maps a realistic path through three phases, from today’s co-pilot and analytics deployments, through portfolio-scale supervisory optimization in the late 2020s, toward bounded autonomy in specific subsystems in the next decade.

Getting there faster depends less on better algorithms than on data infrastructure, smarter delivery models, and an industry willing to hold itself to the independent verification standards that buyers are increasingly demanding.