Reading time: 3 minutes

Smart water metering is no longer defined by the meter alone. What began as a hardware‑led modernization effort is evolving into a data‑centric platform play that reshapes how utilities operate, recover costs, and engage customers. Across regions, the market is moving beyond automated meter reading toward integrated systems that combine connectivity, data management, analytics, and outcome‑based service delivery.

This transformation is driven by a convergence of pressures. Utilities face rising water stress, persistent non‑revenue water, aging infrastructure, and increasing regulatory scrutiny. At the same time, digital technologies such as LPWAN connectivity, advanced meter data management, and analytics platforms are becoming more accessible and scalable. Together, these forces are accelerating the shift from isolated meter deployments to end‑to‑end smart water metering ecosystems.

From Meter Hardware to Integrated Systems

At the core of smart water metering is an increasingly interconnected value architecture. Modern deployments span multiple layers, including smart meters, communication networks, head‑end systems, meter data management platforms, customer engagement portals, and analytics engines. While meter hardware still represents the largest share of market revenue today, much of the long‑term value creation is moving upstream into software, connectivity, and services.

This shift reflects how utilities now view smart metering investments. Rather than treating meters as one‑time capital assets, utilities are using smart metering as a foundation for broader digital transformation. Continuous data flows enable utilities to improve billing accuracy, detect leaks earlier, optimize asset performance, and engage customers more effectively around consumption and conservation.

AMI as the Anchor for Market Growth

Across Europe, Asia‑Pacific, the Middle East and Africa, and the United States, advanced metering infrastructure has emerged as the primary growth engine for smart water metering. Large‑scale AMI rollouts are driving replacement demand for mechanical meters while creating long‑term opportunities for recurring revenue tied to networks, data platforms, and analytics.

In mature markets, AMI programs are often linked to regulatory mandates, loss reduction targets, or national digital utility strategies. In emerging markets, AMI adoption is increasingly tied to performance‑based contracts and public‑sector funding aimed at improving operational efficiency and financial sustainability. In both cases, AMI enables utilities to move beyond manual or semi‑automated processes toward real‑time visibility and control.

Regional Dynamics Shape Adoption Pathways

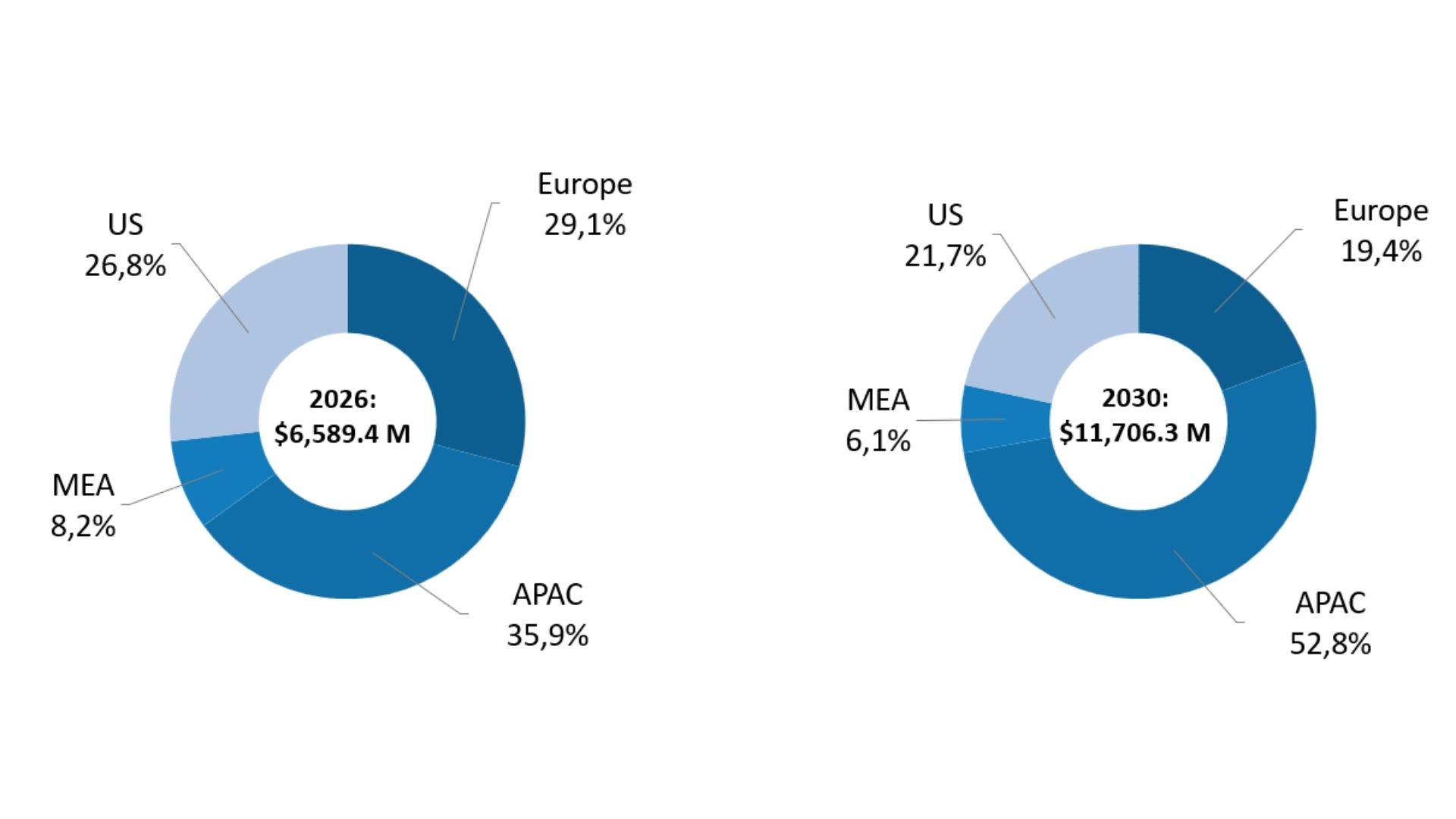

While the strategic direction is consistent globally, regional adoption patterns vary significantly. Europe continues to benefit from strong regulatory alignment, mature technology ecosystems, and utility‑led programs focused on efficiency and sustainability. Asia‑Pacific stands out as the fastest‑growing region, driven by large national rollouts, rapid urbanization, and strong government involvement. China and India contribute scale, while Southeast Asia, Australia, and New Zealand are increasingly focused on loss reduction and conservation.

In the Middle East and Africa, severe water scarcity and intermittent supply conditions shape technology choices. Prepaid meters, static meters with valve control, and analytics‑led NRW reduction solutions are gaining traction, particularly in the GCC and parts of Sub‑Saharan Africa. In the United States, federal and state funding is accelerating replacement cycles, with utilities increasingly favoring AMI‑centric and service‑led deployment models.

Smart Water Metering: Revenue Share Forecast, Selected Regions, 2026 and 2030

Monetization Shifts Toward Services and Outcomes

One of the most significant changes in the smart water metering market is how solutions are being commercialized. Traditional capital‑intensive procurement models are giving way to as‑a‑service and performance‑based approaches. Network‑as‑a‑Service, Metering‑as‑a‑Service, and bundled delivery models reduce upfront costs while transferring technology and operational risk away from utilities.

These models align well with utility priorities, particularly where internal skills are constrained or balance sheet flexibility is limited. For vendors and integrators, they create longer‑term revenue visibility and stronger customer relationships, but also require deeper operational capabilities and financial discipline.

Analytics as the Differentiator

As smart metering deployments mature, analytics is emerging as a key point of differentiation. Meter data management platforms are increasingly positioned as the core intelligence layer that supports leakage detection, consumption profiling, demand forecasting, and regulatory reporting. Utilities are moving beyond basic data collection toward actionable insights that directly support operational and financial outcomes.

Over time, analytics‑led services are expected to play a larger role in monetization, particularly as utilities seek measurable improvements in non‑revenue water reduction, billing efficiency, and customer satisfaction.

Looking Ahead

Smart water metering is transitioning from a technology upgrade to a strategic enabler of digital utility operations. While meter hardware will continue to anchor deployments, the next phase of growth will be defined by connectivity, data platforms, analytics, and service‑based delivery models. Vendors that can integrate across these layers and align offerings with utility outcomes will be best positioned to capture long‑term value as the market continues to evolve.

Download

Additional market data, regional insights, and revenue forecasts are available for download, offering deeper insights into market structure, dynamics, and growth drivers.